Executive Summary

Industrial real estate has emerged as one of the most actively discussed segments of the private real estate market over the past decade. Driven by e-commerce growth, supply chain modernization, manufacturing reshoring, and increased institutional investment, industrial assets have attracted significant capital from both public and private market investors. However, the industrial real estate market is often viewed too narrowly through the lens of logistics facilities and distribution centers, overlooking a broader universe of manufacturing plants, owner-occupied facilities, and specialized industrial properties that operate outside traditional leasing markets.

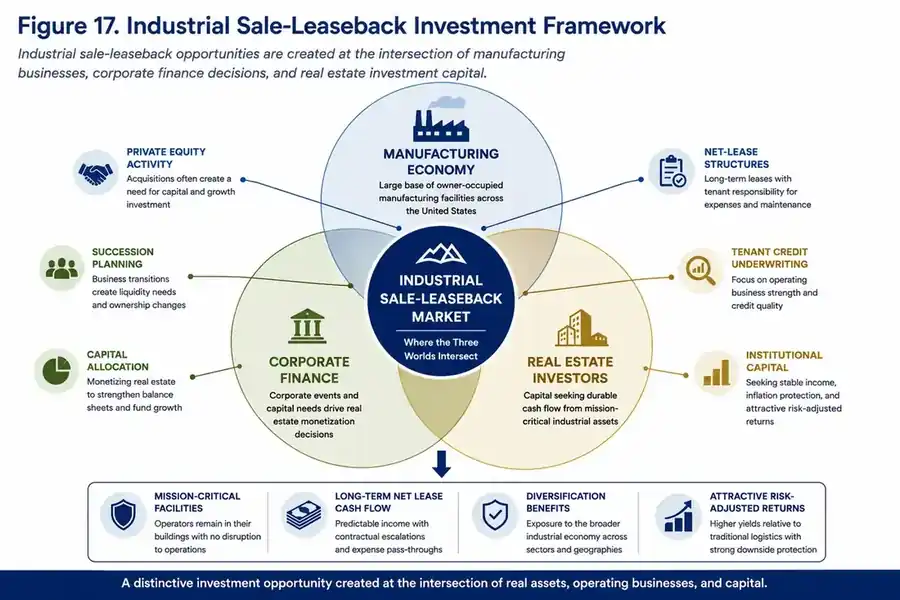

This paper examines industrial real estate from a broader perspective, focusing on the intersection of real estate ownership, corporate finance, and capital allocation. Particular attention is given to manufacturing facilities and industrial sale-leaseback transactions, which represent a distinct segment of the industrial market that differs materially from institutional logistics investing.

A central observation of this research is that a significant portion of U.S. manufacturing real estate remains owner-occupied. While traditional industrial market reports focus primarily on leased inventory, vacancy rates, and leasing activity, many manufacturing businesses continue to own the facilities from which they operate. As a result, a large segment of industrial real estate exists outside the datasets commonly used by institutional investors and market analysts.

The sale-leaseback market has developed as a mechanism for converting these owner-occupied facilities into sources of corporate capital. Through a sale-leaseback transaction, an operating company sells its real estate to an investor while simultaneously entering into a long-term lease to continue operating from the property. This structure allows businesses to unlock capital tied up in real estate ownership while preserving operational continuity.

For investors, industrial sale-leasebacks offer exposure to long-term lease structures, mission-critical facilities, and potentially higher stated yields than those available in more institutionalized segments of the industrial market. These opportunities, however, often require a deeper understanding of tenant credit, facility specialization, geographic concentration, and capital markets dynamics than traditional industrial investments.

The research further explores the role of private equity in industrial sale-leaseback transactions. In many cases, industrial real estate transactions occur alongside business acquisitions, recapitalizations, ownership transitions, and other corporate events. As a result, the industrial sale-leaseback market often sits at the intersection of real estate investing, corporate finance, and private equity strategy.

Valuation remains one of the most important and frequently misunderstood aspects of the sector. Industrial assets that appear similar on the surface may trade at substantially different capitalization rates depending on tenant quality, market location, lease structure, building flexibility, and buyer competition. Higher cap rates commonly observed in manufacturing-focused sale-leaseback transactions may reflect a combination of increased risk, lower liquidity, and reduced investor competition rather than simple market inefficiency.

Ultimately, industrial sale-leasebacks represent a specialized segment of private real estate investing that may present potential opportunities for investors willing to undertake deeper underwriting of operating businesses, real estate assets, and transaction structures. Understanding the ownership dynamics, valuation frameworks, and risk factors that define this market is essential for evaluating investment opportunities within the sector.

2. Industrial Real Estate Landscape

2.1 Defining Industrial Real Estate

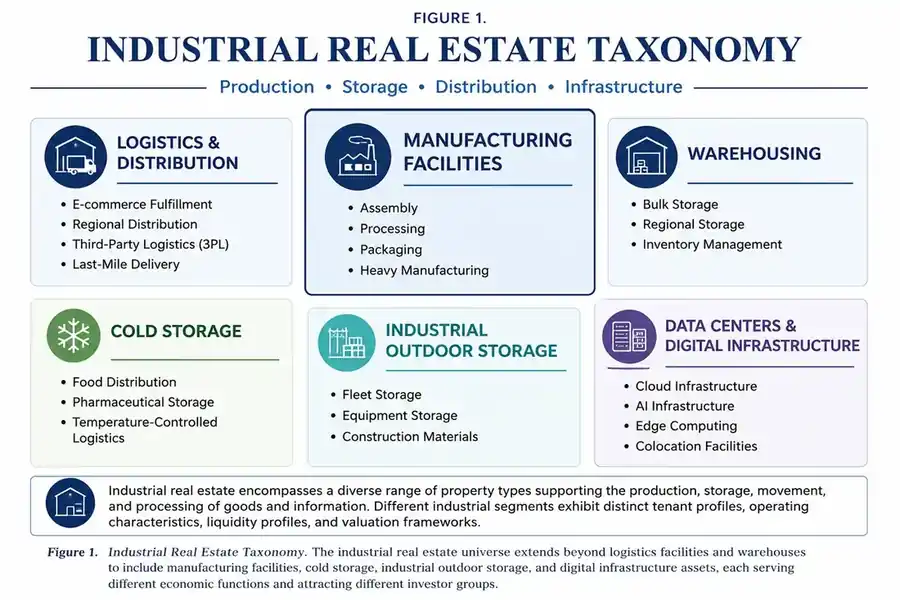

Industrial real estate is one of the largest and most diverse segments of the commercial property market. Broadly defined, industrial properties are facilities used for manufacturing, production, storage, distribution, assembly, processing, transportation, and related business activities.

Unlike office, retail, or multifamily real estate, industrial assets support the movement, transformation, and production of goods throughout the economy. As a result, industrial real estate serves as a critical component of supply chains, manufacturing systems, and distribution networks.

The sector encompasses a wide range of property types, including logistics warehouses, distribution centers, manufacturing plants, cold storage facilities, industrial outdoor storage properties, and specialized facilities designed around specific production processes.

Although these assets are often grouped together under the umbrella of "industrial real estate," their economics, risk profiles, tenant bases, and valuation characteristics can vary significantly.

Key categories include:

- Logistics and Distribution Facilities

These properties are designed primarily for storage and movement of goods. Tenants typically include e-commerce companies, third-party logistics providers, retailers, and transportation firms. Logistics facilities have attracted substantial institutional investment due to strong demand growth, operational flexibility, and relatively deep buyer pools.

Warehousing

Traditional warehouse facilities provide storage space for inventory and goods. While often grouped with logistics assets, warehouses vary substantially in quality, location, and tenant profile.

Manufacturing Facilities

Manufacturing facilities are used to produce, assemble, process, or package goods. These properties often contain specialized improvements, customized layouts, heavy power infrastructure, or production equipment designed for specific business operations.

Manufacturing facilities are particularly important to this research because a substantial portion remain owner-occupied rather than leased.

Cold Storage Facilities

Cold storage assets provide temperature-controlled environments used by food distributors, pharmaceutical companies, and other industries requiring specialized storage conditions. These facilities often command distinct valuation characteristics due to their operational complexity and infrastructure requirements.

Industrial Outdoor Storage (IOS)

Industrial outdoor storage properties consist primarily of land used for equipment storage, vehicle fleets, construction materials, and other industrial purposes. Although historically overlooked by institutional investors, IOS has become an increasingly recognized industrial subsector.

Data Centers and Digital Infrastructure

Data centers are frequently grouped within industrial real estate due to their physical infrastructure characteristics. However, their economics are often driven by power capacity, connectivity, and computing demand rather than traditional industrial factors. For this reason, data centers are increasingly analyzed as a distinct category of digital infrastructure.

2.2 Not All Industrial Assets Are Created Equal

One of the most common misconceptions in commercial real estate is that industrial properties represent a homogeneous asset class.

In reality, industrial assets vary dramatically in terms of:

- Tenant profile

- Lease structure

- Building flexibility

- Geographic location

- Capital requirements

- Exit liquidity

- Institutional demand

A newly constructed logistics facility leased to a national e-commerce tenant in a major distribution hub differs substantially from a specialized manufacturing facility occupied by a middle-market industrial company in a secondary market. Although both assets fall within the industrial category, investors may apply entirely different underwriting frameworks and valuation methodologies.

These differences become particularly important when evaluating industrial sale-leaseback transactions, where tenant quality and facility utility often play a larger role than conventional real estate metrics.

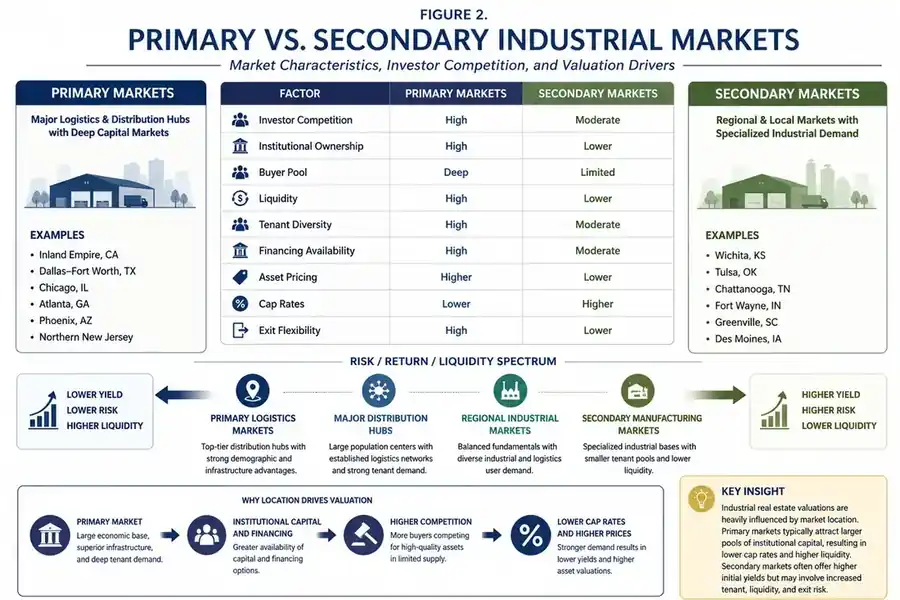

2.3 Primary and Secondary Industrial Markets

Industrial real estate markets are commonly divided into primary, secondary, and tertiary markets.

Primary Markets

Primary markets typically feature:

- Large populations

- Extensive transportation infrastructure

- Deep labor pools

- Significant institutional ownership

- Strong liquidity

- Examples include:

- Inland Empire, California

- Dallas-Fort Worth, Texas

- Chicago, Illinois

- Atlanta, Georgia

- Phoenix, Arizona

- Northern New Jersey

These markets generally attract substantial institutional capital and often exhibit lower capitalization rates due to strong investor demand.

Secondary Markets

Secondary markets tend to be smaller metropolitan areas with meaningful industrial activity but less institutional ownership and liquidity.

Examples may include:

- Wichita, Kansas

- Tulsa, Oklahoma

- Chattanooga, Tennessee

- Fort Wayne, Indiana

- Greenville, South Carolina

Secondary markets frequently support manufacturing operations and specialized industrial businesses. Because investor competition is often lower, assets in these markets may trade at higher capitalization rates.

The distinction between primary and secondary markets becomes increasingly important throughout this paper because many manufacturing-focused sale-leaseback transactions occur outside the large logistics hubs that dominate institutional industrial investing.

2.4 Institutional Ownership and Market Evolution

Industrial real estate has undergone a significant transformation over the past two decades.

Historically, institutional investors allocated substantial capital to office buildings, multifamily housing, and retail properties. Industrial assets were often viewed as operationally intensive and less prominent than other commercial property types.

This perception began to change as e-commerce growth accelerated and supply chains became increasingly dependent on sophisticated logistics networks. Large institutional investors recognized the strategic importance of distribution infrastructure and deployed significant capital into modern industrial facilities.

Today, some of the world's largest real estate investment platforms maintain substantial industrial portfolios. These investors typically focus on logistics facilities, distribution centers, and other highly liquid industrial assets capable of supporting large-scale portfolio construction.

At the same time, many manufacturing facilities remain outside institutional ownership structures, creating a distinct segment of the market that continues to be served primarily through direct ownership, sale-leaseback transactions, and specialized industrial investment strategies.

2.5 Key Observations

Several themes emerge from the industrial real estate landscape.

First, industrial real estate should not be viewed as a single asset class. Different industrial subsectors exhibit different economic drivers, risk characteristics, and investor participation levels.

Second, manufacturing facilities occupy a unique position within the industrial ecosystem. Unlike logistics assets that have become heavily institutionalized, many manufacturing facilities remain owner-occupied and underrepresented in traditional market statistics.

Third, location matters. Primary and secondary markets often attract different investor groups and command different valuations, even when assets appear similar from an operational perspective.

Finally, the continued evolution of manufacturing, logistics, supply chains, and digital infrastructure suggests that industrial real estate will remain one of the most dynamic segments of the private real estate market for years to come.

The next section examines one of the least visible yet potentially most important components of this market: owner-occupied manufacturing facilities.

3. Manufacturing Facility Ownership: The Hidden Market

3.1 Looking Beyond Traditional Industrial Market Statistics

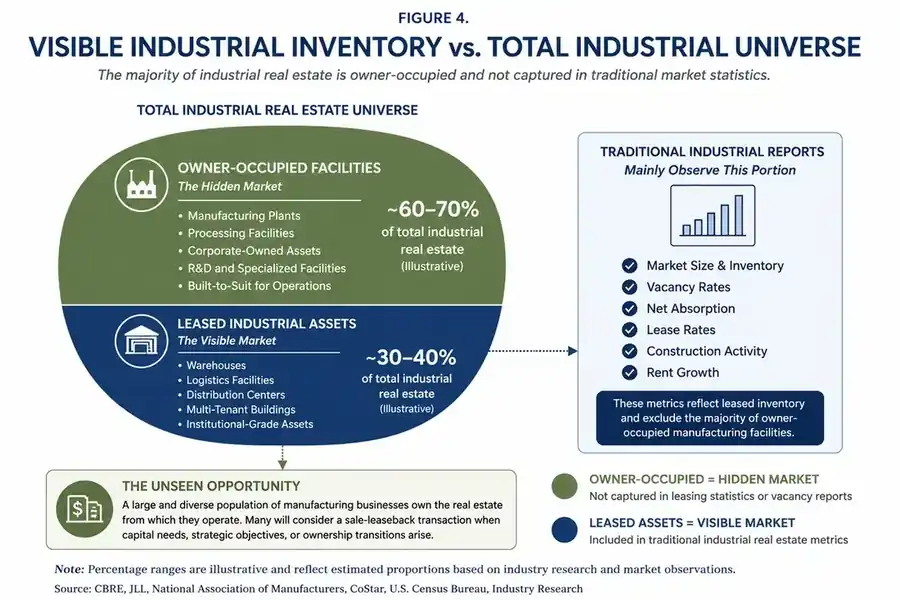

Most industrial real estate research begins with familiar metrics: vacancy rates, absorption, leasing activity, rental growth, and transaction volume. These measures are useful for understanding the visible portion of the industrial market, particularly logistics facilities, warehouses, and other properties that actively participate in leasing markets. However, they may provide only a partial view of the broader industrial real estate universe.

A significant portion of American manufacturing activity takes place in facilities owned by the businesses that occupy them. These owner-occupied properties frequently fall outside traditional leasing statistics and are often underrepresented in institutional market reports. As a result, investors focusing exclusively on leased industrial inventory may overlook a substantial segment of industrial real estate ownership.

This distinction is important because industrial sale-leaseback opportunities originate not from leased properties but from owner-occupied properties. Understanding who owns industrial facilities—and why they continue to own them—provides important context for understanding the sale-leaseback market itself.

The purpose of this section is therefore not simply to analyze manufacturing. Rather, it is to examine the ownership structure of manufacturing real estate and explain why that ownership structure creates a distinct opportunity set for industrial real estate investors.

3.2 The Scale of the U.S. Manufacturing Base

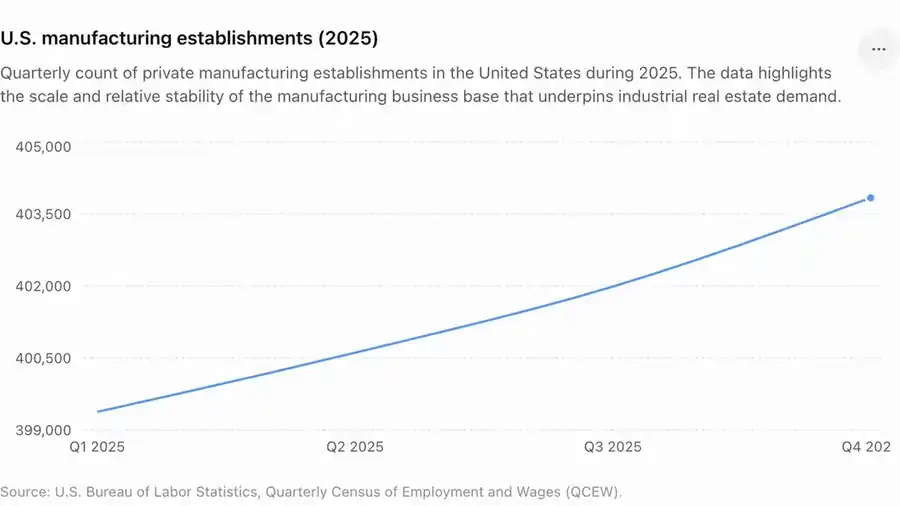

The United States remains one of the world's largest manufacturing economies. Although public attention often focuses on technology, financial services, and consumer industries, manufacturing continues to represent a significant component of the American economic landscape.

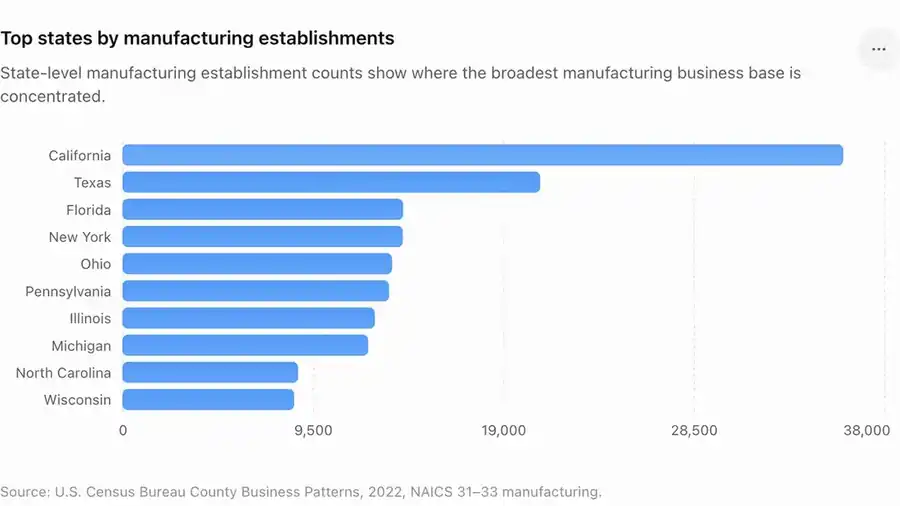

More than 400,000 manufacturing establishments operate across the country, spanning industries such as aerospace, food processing, medical devices, industrial machinery, packaging, chemicals, electronics, transportation equipment, and countless specialized production activities.

Figure 3 illustrates the scale of the U.S. manufacturing sector, with more than 400,000 manufacturing establishments operating nationwide during 2025. While individual facilities vary significantly in size, industry, and ownership structure, the chart demonstrates the breadth of the operating business base that ultimately drives demand for industrial real estate. Importantly, many of these establishments occupy facilities that are owned by the operating company rather than leased from institutional real estate investors, creating a large universe of industrial properties that may not be fully reflected in traditional leasing-market statistics.

3.3 Why So Many Manufacturers Continue to Own Their Facilities

One of the defining characteristics of the manufacturing sector is the persistence of owner-occupied real estate.

Historically, many manufacturers acquired or developed facilities for long-term operational purposes rather than investment purposes. Ownership provided stability, control, and the ability to customize facilities around production requirements without relying on third-party landlords. Over time, these facilities often became integral components of the business itself.

In many cases, industrial properties were acquired decades ago when land values and construction costs were substantially lower than they are today. As businesses grew, real estate ownership remained embedded within the operating company rather than being separated into a dedicated real estate structure.

The result is that many successful manufacturing businesses simultaneously own two valuable assets: the operating enterprise and the real estate from which the enterprise operates.

This ownership structure differs materially from sectors such as retail, hospitality, and logistics, where lease-based occupancy models have become increasingly common.

3.4 The Invisible Portion of the Industrial Market

One of the challenges facing industrial real estate research is that comprehensive ownership data remains surprisingly difficult to obtain.

Most market reports focus on leased inventory because those assets generate observable market data. Analysts can track vacancy rates, lease transactions, rental growth, tenant demand, and investment sales activity. Owner-occupied properties, by contrast, often generate far less public information.

As a result, the industrial market visible through leasing statistics may represent only a portion of the total industrial property universe.

The distinction illustrated in Figure 4 is central to this paper. Traditional industrial market research primarily observes leased assets, while industrial sale-leaseback investors frequently target facilities that may never appear in conventional leasing datasets. In effect, the sale-leaseback market draws opportunities from a pool of properties that is partially hidden from traditional real estate analysis.

This observation helps explain why industrial sale-leaseback investors often approach the market differently than conventional industrial investors. Their opportunity set originates not from available buildings but from existing business ownership.

3.5 Capital Embedded in Industrial Real Estate

The prevalence of owner-occupied facilities creates an important capital allocation question.

A manufacturing company may own a facility worth tens or even hundreds of millions of dollars while simultaneously pursuing growth initiatives that require additional capital. Expansion projects, equipment modernization, acquisitions, automation initiatives, and working capital needs all compete for corporate resources.

The real estate itself may represent a substantial source of embedded value that remains largely inaccessible unless the company sells, refinances, or otherwise monetizes the asset.

This dynamic is one of the primary reasons sale-leasebacks have become increasingly attractive. Rather than viewing real estate ownership as a permanent feature of the business, many owners and investors now evaluate whether capital tied up in real estate could be deployed more effectively elsewhere.

The question is not whether the facility is important. In most cases, the facility remains absolutely critical to operations. The question is whether ownership of the facility generates greater value than alternative uses of that capital.

3.6 Geographic Concentration and Manufacturing Ownership

Manufacturing ownership patterns are also influenced by geography.

Many of the regions traditionally associated with American manufacturing developed their industrial infrastructure over multiple generations. States such as Ohio, Michigan, Indiana, Pennsylvania, Wisconsin, and Illinois contain large concentrations of legacy manufacturing facilities that were often constructed under long-term ownership models.

At the same time, manufacturing activity has expanded significantly across portions of the South and Southwest. Texas, Tennessee, South Carolina, Arizona, and other growth markets have attracted substantial manufacturing investment over the past several decades, often supported by favorable business climates, infrastructure development, and workforce availability.

California and Texas lead the United States by manufacturing establishment count, followed by a dense group of major industrial states across the Southeast, Northeast, and Midwest. Establishment counts are useful for identifying the breadth of the manufacturing operating base, but they should not be confused with output, employment, or facility size.

Establishment count measures the number of reported manufacturing business locations, not the number of facilities owned by operating companies. Ownership structure must be evaluated separately.

3.7 The Hidden Opportunity Set

The most important conclusion from this section is that industrial real estate can be analyzed from two fundamentally different perspectives.

Traditional industrial investors often begin with buildings. They study vacancy rates, leasing trends, rent growth, and property transactions in order to identify attractive opportunities.

Sale-leaseback investors often begin with businesses. They focus on ownership structures, capital needs, succession planning, acquisitions, recapitalizations, and other corporate events that may ultimately lead to real estate transactions.

This distinction creates a different sourcing model and, potentially, a different opportunity set.

Rather than competing solely for assets already available in the investment market, sale-leaseback investors may gain access to properties that have never been marketed for sale and may not even be viewed as investment properties by their current owners.

The scale of the manufacturing sector suggests that this opportunity set may be substantially larger than conventional industrial market statistics imply.

3.8 Key Observations

The United States maintains a large and diverse manufacturing base supported by hundreds of thousands of operating establishments. A significant portion of these businesses continue to occupy facilities they own rather than lease, creating a substantial pool of industrial real estate that exists outside many traditional leasing-market datasets.

This ownership structure is more than a historical curiosity. It forms the foundation of the industrial sale-leaseback market. Every sale-leaseback transaction begins with an owner-occupied property, and the continued prevalence of owner-occupied manufacturing facilities helps explain why opportunities continue to emerge despite growing institutional interest in industrial real estate.

The next section examines how those ownership structures are converted into investment opportunities through sale-leaseback transactions and why real estate monetization has become an increasingly important capital allocation strategy for operating businesses.

4. Sale-Leaseback as a Capital Release Strategy

4.1 Introduction

The ownership structure described in the prior section creates an important corporate finance question: if a manufacturing business owns the facility from which it operates, should that real estate remain on the company’s balance sheet, or can the capital tied up in the property be redeployed into higher-return operating uses?

A sale-leaseback transaction provides one answer to that question.

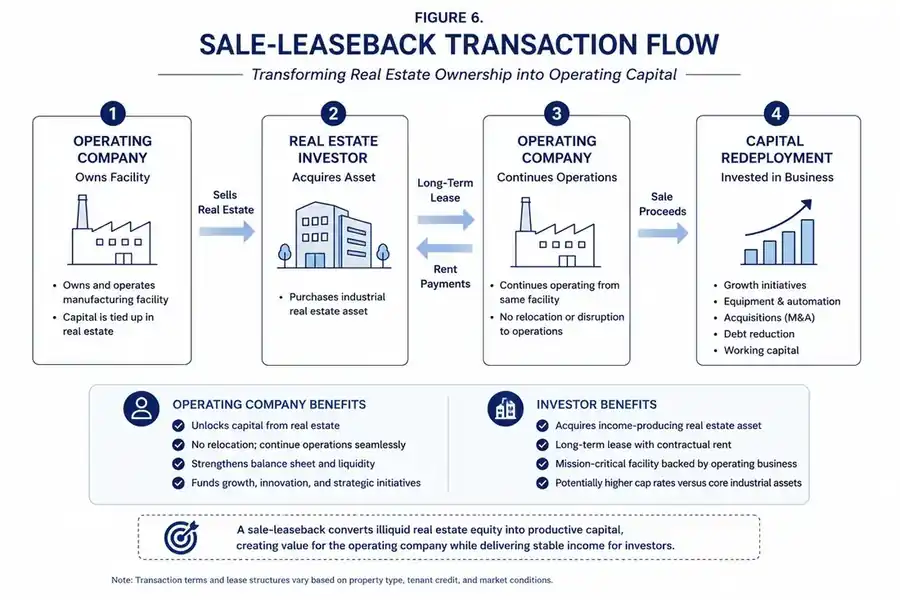

In a sale-leaseback, an owner-occupier sells its real estate to an investor and simultaneously enters into a long-term lease to continue operating from the same facility. The operating company becomes the tenant, while the purchaser becomes the landlord. In many cases, the lease is structured as a net lease, meaning the tenant remains responsible for some or all property-level expenses, including taxes, insurance, and maintenance.

This structure allows the business to monetize an illiquid real estate asset while preserving operational continuity. For investors, the transaction creates an income-producing real estate asset backed by a long-term lease.

4.2 Transaction Structure

A sale-leaseback is best understood as a financing transaction secured by operating real estate, rather than simply a property sale.

The basic structure is straightforward:

- Step 1: The operating company owns and occupies a facility.

- Step 2: The company sells the property to a real estate investor.

- Step 3: The company signs a long-term lease and continues operating from the same location.

- Step 4: The sale proceeds are redeployed into the business or used for another corporate purpose.

- Step 5: The investor receives rental income under the lease.

Northmarq describes the structure as one where an owner-occupant sells its property and immediately enters into a long-term lease agreement to rent the property from the new owner. The lease governs the tenancy, rental rate, duration, and property expense responsibilities.

In a sale-leaseback transaction, an operating company sells its facility to a real estate investor and simultaneously enters into a long-term lease. The company continues operating from the same location while redeploying sale proceeds into business initiatives such as growth, acquisitions, equipment investment, or debt reduction. For investors, the transaction creates an income-producing real estate asset backed by an operating business tenant.

4.3 Corporate Finance Perspective

For the operating company, a sale-leaseback converts real estate ownership into liquidity.

This distinction is important. A manufacturing company may own a valuable facility, but that value may not directly support growth unless the company sells, refinances, or otherwise monetizes the asset. Sale-leasebacks allow companies to convert an illiquid real estate asset into capital that can be used for operating purposes.

Plante Moran describes sale-leasebacks as a way for business owners to unlock capital by converting an illiquid real estate asset into funds that can be deployed into growth initiatives, balance sheet improvement, high-return business segments, stock buybacks, or M&A financing.

Common uses of proceeds include:

- The central capital allocation question is simple:

Can the company generate a higher return by reinvesting the capital into the business than by continuing to own the real estate?

For many manufacturers, the answer may depend on growth opportunities, financing costs, equipment needs, succession planning, and ownership objectives.

4.4 Why Sale-Leasebacks May Be Attractive to Manufacturers

Manufacturing businesses are often capital-intensive. Facilities may require substantial investment in equipment, production lines, power infrastructure, environmental controls, inventory systems, and specialized improvements.

At the same time, many manufacturers operate from properties purchased or developed years earlier. Over time, those properties may appreciate significantly, creating real estate equity that remains trapped on the balance sheet.

A sale-leaseback may be relevant when the company wants to:

- preserve use of the facility;

- avoid operational disruption;

- access capital without relocating;

- shift real estate ownership to a financial investor;

- focus management attention on the operating business;

redeploy capital into higher-return uses.

The transaction may be especially relevant when the facility is mission-critical but real estate ownership itself is not a core competency of the business.

In other words, the company may need the facility, but it may not need to own the facility.

4.5 Investor Perspective

For the real estate investor, the sale-leaseback creates a long-term income stream tied to an operating business.

The appeal often comes from the combination of:

- long lease duration;

- contractual rent payments;

- net lease expense structure;

- mission-critical real estate;

- potential annual rent escalators;

higher cap rates than more liquid institutional assets.

However, these benefits come with trade-offs. In many sale-leaseback transactions, the investor is not only underwriting the building. The investor is also underwriting the tenant’s business.

This creates a hybrid investment profile.

The value of the property may depend heavily on the tenant’s ability to continue operating profitably from the facility.

4.6 Sale-Leaseback vs. Traditional Debt Financing

Sale-leasebacks often compete with traditional financing alternatives.

A company seeking capital may consider:

- mortgage financing;

- asset-based lending;

- senior secured debt;

- mezzanine debt;

- equity capital;

sale-leaseback financing.

Each option has different implications for ownership, control, leverage, and flexibility.

W. P. Carey notes that sale-leasebacks can allow private equity firms and portfolio companies to extract value from real estate and convert otherwise illiquid property into working capital while maintaining operational control.

This distinction is important for manufacturers because the sale-leaseback may release more capital than a conventional mortgage, but it also involves giving up ownership and committing to a long-term lease.

4.7 Why the Lease Structure Matters

The lease is the core economic document in a sale-leaseback transaction.

Important lease terms include:

- initial lease term;

- renewal options;

- rent escalators;

- tenant expense obligations;

- maintenance responsibilities;

- assignment rights;

- change-of-control provisions;

- default remedies;

purchase options, if any.

For investors, the lease determines the durability of income. For the operating company, the lease determines long-term occupancy cost and operational flexibility.

A facility may be mission-critical today, but investors must also evaluate whether it is likely to remain mission-critical throughout the lease term.

4.8 Strategic Growth, Not Just Distress Financing

A common misconception is that sale-leasebacks are primarily used by distressed companies.

In practice, sale-leasebacks may be used by healthy companies seeking to fund growth, acquisitions, expansion, modernization, or shareholder liquidity. Northmarq notes that many sale-leasebacks are motivated by strategic growth initiatives, including new market entry, unit development, and M&A financing, rather than financial distress.

This distinction is particularly relevant in manufacturing. A company may own valuable real estate but face attractive opportunities to invest in automation, capacity expansion, or acquisitions. In such cases, real estate monetization may be a deliberate capital allocation decision rather than a sign of financial weakness.

4.9 Implications for Industrial Real Estate Investors

The sale-leaseback model changes the investor’s sourcing process.

Traditional industrial investors often begin with the property market:

- available buildings;

- leasing activity;

- vacancy rates;

- rent growth;

comparable sales.

Sale-leaseback investors often begin with the operating business:

- company ownership;

- capital needs;

- facility importance;

- industry outlook;

- tenant credit;

- private equity activity;

succession planning.

This distinction is central to understanding the industrial sale-leaseback market.

Traditional industrial investing often starts with buildings.

Industrial sale-leaseback investing often starts with businesses.

4.10 Key Takeaways

Sale-leasebacks convert owner-occupied industrial real estate into a source of corporate capital while allowing the operating company to remain in place.

For manufacturers, the structure can provide liquidity for growth, M&A, equipment investment, debt reduction, or ownership transition planning.

For investors, the strategy can create long-term income exposure to mission-critical facilities, but underwriting must account for tenant credit, facility specialization, lease terms, and exit liquidity.

The sale-leaseback market therefore sits at the intersection of real estate investing and corporate finance.

The next section examines a related and increasingly important source of transaction activity: private equity-sponsored acquisitions and recapitalizations.

5. Private Equity and Sale-Leaseback Partnerships

5.1 The Growing Connection Between Private Equity and Industrial Real Estate

The industrial sale-leaseback market has become increasingly intertwined with private equity activity over the past two decades. While sale-leaseback transactions historically occurred as standalone corporate finance events, many contemporary transactions originate from ownership transitions, recapitalizations, and private equity-sponsored acquisitions.

This relationship exists because industrial real estate frequently represents a significant asset on the balance sheet of middle-market manufacturing businesses. When private equity firms acquire operating companies, they often inherit both the operating enterprise and the real estate from which that enterprise conducts its activities. As a result, sponsors must determine whether retaining ownership of the real estate contributes to the overall investment strategy or whether capital can be deployed more effectively elsewhere.

In many situations, the real estate itself is not the primary investment objective. Private equity sponsors are generally seeking to improve operational performance, increase earnings, pursue acquisitions, expand market share, or execute other strategic initiatives that enhance the value of the operating company. Real estate ownership may support those objectives, but it may also represent capital that could potentially be redeployed into higher-return business activities.

5.2 The Three-Party Ecosystem

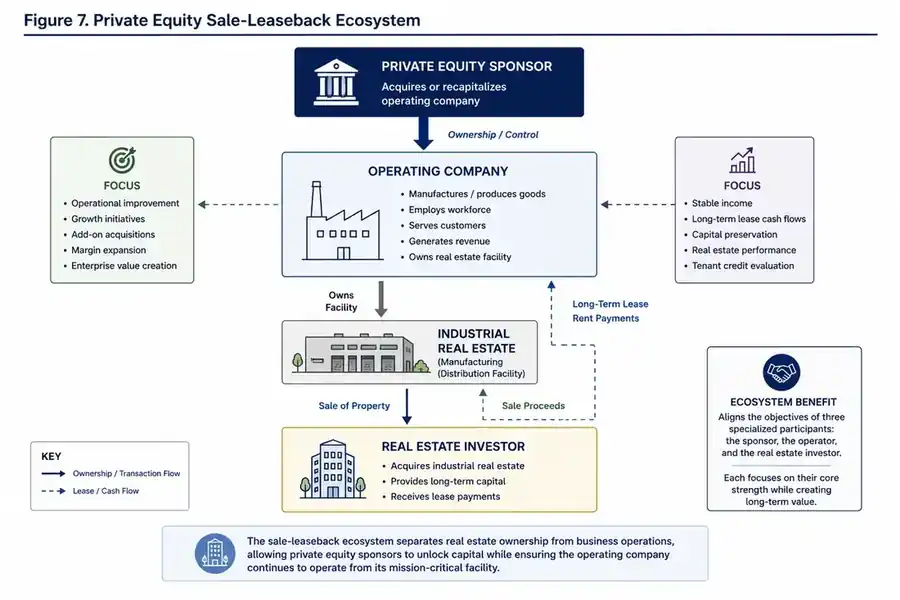

A distinctive feature of many industrial sale-leaseback transactions is the presence of three separate stakeholders: the operating company, the private equity sponsor, and the real estate investor. Each participant enters the transaction with different objectives and expertise.

The operating company requires continued access to the facility in order to manufacture products, serve customers, and generate revenue. The private equity sponsor seeks to maximize enterprise value and optimize capital allocation across the business. The real estate investor focuses on acquiring an income-producing asset supported by a long-term lease and an operating tenant.

The resulting transaction structure allows each participant to focus on its core competency. The operating company continues running the business, the sponsor concentrates on value creation, and the real estate investor assumes responsibility for ownership of the property.

5.3 Why Private Equity Sponsors Utilize Sale-Leasebacks

For private equity firms, sale-leasebacks are often a capital allocation tool rather than a real estate strategy. Following an acquisition, sponsors frequently evaluate whether capital invested in owned real estate could generate higher returns if deployed elsewhere within the business.

Sale-leaseback proceeds may be used to fund acquisitions, support organic growth initiatives, expand production capacity, modernize equipment, reduce leverage, or provide liquidity as part of a recapitalization. In many cases, the transaction allows a sponsor to unlock capital while maintaining uninterrupted use of a mission-critical facility.

The decision ultimately reflects a broader investment principle: capital should generally be allocated toward activities that generate the highest risk-adjusted returns. If a manufacturing company can earn materially higher returns by investing in its operations than by owning real estate, monetizing the property may represent an economically rational decision.

5.4 Implications for Real Estate Investors

From the perspective of a real estate investor, private equity-sponsored transactions can present unique opportunities. Unlike traditional property acquisitions marketed through brokerage channels, many sale-leaseback opportunities originate directly from corporate events and ownership transitions.

This sourcing dynamic can create access to properties that might never appear in the conventional transaction market. Investors may also benefit from enhanced financial reporting, stronger governance practices, and growth-oriented business plans often associated with institutional ownership structures.

However, investors must be careful not to assume that private equity ownership automatically translates into lower risk. The financial health of the tenant, industry conditions, leverage levels, and long-term business viability remain critical underwriting considerations regardless of ownership structure.

5.5 Does Private Equity Ownership Improve Tenant Quality?

One of the most interesting questions in the sale-leaseback market is whether private equity ownership improves tenant quality and lease security.

There are arguments supporting both sides of this question. On one hand, private equity sponsors often bring capital, professional management, strategic planning, and operational expertise that may strengthen a company's competitive position. Portfolio companies may gain access to resources that would otherwise be unavailable to independently owned businesses.

On the other hand, private equity ownership may introduce additional leverage, aggressive growth strategies, or ownership turnover. The financial objectives of a sponsor do not always align perfectly with the objectives of a long-term real estate investor.

As a result, evaluating tenant quality requires analysis of the operating business itself rather than relying solely on sponsor reputation. The presence of a private equity owner may be a positive factor, but it should not replace fundamental credit analysis.

5.6 Capital Flows in Private Equity-Sponsored Sale-Leasebacks

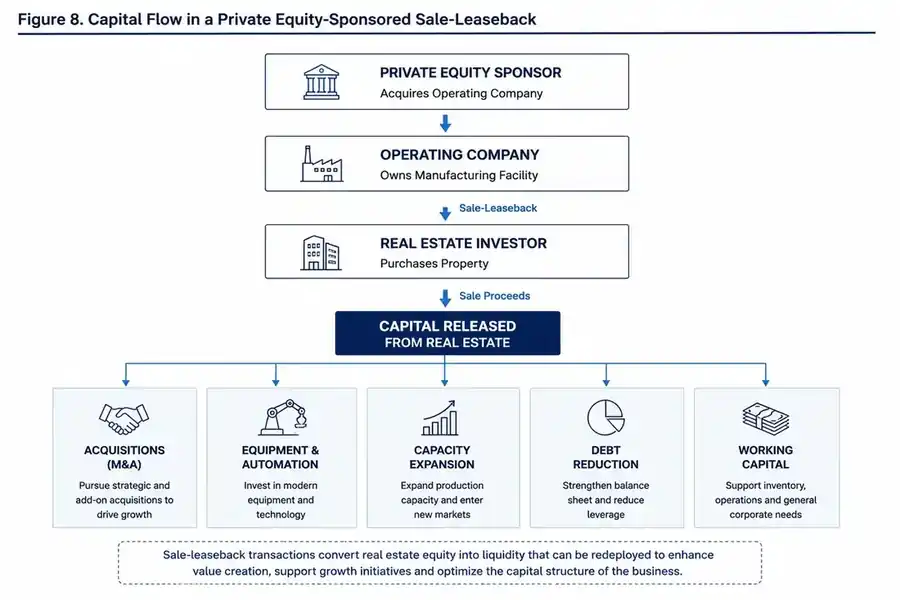

The financial mechanics of these transactions help explain their growing popularity. Real estate that may have accumulated on a company's balance sheet over decades can be converted into capital that supports future growth.

The flow of capital typically begins with an acquisition or recapitalization event. Following the transaction, the operating company monetizes its real estate through a sale-leaseback. The resulting proceeds are then redeployed into business initiatives, acquisitions, debt reduction, or other strategic priorities.

Following a sale-leaseback transaction, capital previously tied up in real estate ownership may be redeployed into strategic business initiatives. Common uses include acquisitions, equipment modernization, capacity expansion, debt reduction, and working capital support. This ability to redirect capital toward operating priorities is one of the primary reasons sale-leasebacks are frequently utilized in private equity-sponsored transactions.

5.7 Key Observations

The increasing overlap between private equity and industrial real estate has become an important driver of sale-leaseback activity. Many opportunities emerge not because a property owner wishes to sell real estate, but because a broader corporate transaction creates an opportunity to separate operating assets from property ownership.

For investors, understanding ownership transitions, recapitalizations, acquisitions, and succession planning may therefore be as important as understanding traditional industrial market fundamentals. In many cases, the catalyst for a sale-leaseback transaction is a business event rather than a real estate event.

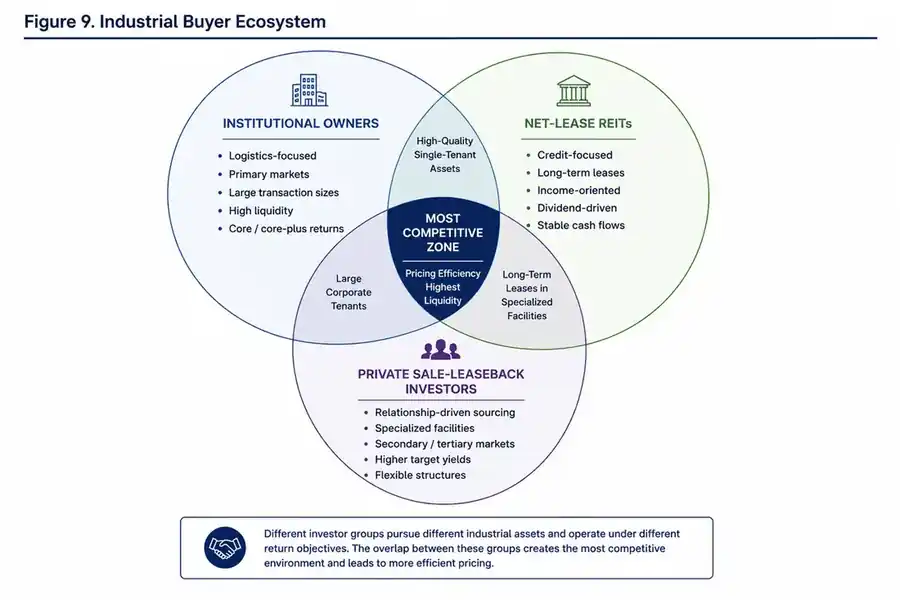

6. Market Participants and Competitive Landscape

6.1 The Evolution of Industrial Real Estate Ownership

Industrial real estate has undergone a profound transformation over the past two decades. Historically viewed as a relatively specialized segment of commercial real estate, industrial properties have become one of the most sought-after asset classes among institutional investors. Growth in e-commerce, supply chain modernization, reshoring initiatives, and logistics infrastructure investment have attracted substantial amounts of capital into the sector.

As industrial real estate has matured, ownership has become increasingly segmented. Large institutional investors, public REITs, private equity firms, sovereign wealth funds, pension funds, and independent sponsors all participate in the market, but they often pursue very different types of opportunities.

As a result, the industrial market is best understood not as a single pool of buyers competing for identical assets, but as a collection of overlapping buyer groups with distinct objectives, underwriting criteria, and return expectations.

Understanding these participants is important because investor demand is one of the primary drivers of industrial property valuations.

6.2 Institutional Industrial Owners

The largest and most visible participants in the industrial market are institutional real estate investors. These firms typically manage billions of dollars of capital on behalf of pension funds, insurance companies, sovereign wealth funds, endowments, and other large investors.

Institutional owners generally seek assets that offer scale, liquidity, and predictable cash flow. Their portfolios often concentrate on major logistics hubs, distribution centers, and modern warehouse facilities located in primary markets.

Examples of major institutional participants include:

- Prologis

- Blackstone

- Brookfield

- GLP

- EQT Exeter

- CBRE Investment Management

- BentallGreenOak

These organizations typically focus on large transactions and portfolio-scale acquisitions. Their investment mandates frequently emphasize geographic diversification, institutional-quality tenants, and properties located in highly liquid markets.

Because these investors control significant amounts of capital, their presence has materially influenced industrial real estate pricing over the past decade. Competition among institutional buyers has compressed cap rates in many primary logistics markets and contributed to substantial appreciation in industrial property values.

For many institutional investors, the primary attraction of industrial real estate lies in logistics infrastructure rather than specialized manufacturing facilities. Modern warehouses and distribution centers often offer greater tenant flexibility, deeper buyer pools, and more predictable exit opportunities than highly specialized industrial assets.

6.3 Public Net-Lease REITs

A second important category of industrial investors consists of public net-lease real estate investment trusts.

Unlike traditional industrial landlords, net-lease investors focus on long-term contractual income streams supported by tenant credit quality. Their investment strategy frequently emphasizes lease structure as much as the underlying real estate itself.

Notable participants include:

- W. P. Carey

- Realty Income

- STAG Industrial

- Essential Properties Realty Trust

- Broadstone Net Lease

These firms often acquire properties through direct transactions with operating companies and are active participants in the sale-leaseback market.

From an underwriting perspective, net-lease investors tend to evaluate both the real estate and the tenant's ability to meet long-term lease obligations. As a result, corporate credit, lease duration, rent escalation provisions, and tenant industry exposure frequently play a central role in investment decisions.

Compared with institutional logistics investors, net-lease REITs are generally more willing to acquire operationally specialized properties when supported by strong tenants and long-term leases.

This distinction has made net-lease REITs important participants in manufacturing-oriented sale-leaseback transactions.

6.4 Private Sale-Leaseback Investors

Beyond institutional owners and public REITs exists a large and often less visible universe of private investors focused on industrial sale-leasebacks.

These participants include:

- Independent sponsors

- Private real estate funds

- Family offices

- Private credit investors

- Specialized industrial investment platforms

- High-net-worth investor syndications

Unlike large institutional investors, private sale-leaseback investors often target opportunities that are too small, too specialized, or too relationship-driven to attract broad institutional competition.

Many of these transactions originate directly from business owners rather than through brokered property sales. The sourcing process frequently involves relationships with business owners, private equity firms, investment bankers, corporate advisors, and regional brokerage networks.

Because these investors often operate outside highly competitive institutional markets, they may be able to acquire assets at cap rates that differ materially from those observed in primary logistics markets.

This segment of the market is particularly relevant to manufacturing-focused sale-leaseback strategies because many owner-occupied facilities fall outside the traditional acquisition criteria of larger institutional buyers.

6.5 Not All Buyers Compete for the Same Assets

One of the most common misconceptions in industrial real estate is that all buyers are competing for the same properties.

In reality, different investor groups often pursue entirely different segments of the market.

An institutional logistics fund may seek a newly constructed distribution center leased to a national tenant in Dallas, Atlanta, or the Inland Empire. A public net-lease REIT may focus on long-term lease structures backed by established operating companies. A private sale-leaseback investor may target a specialized manufacturing facility in a secondary market where institutional competition is limited.

Although all three assets fall under the broad category of industrial real estate, they may attract different buyers, command different cap rates, and exhibit different risk-return profiles.

This segmentation helps explain why industrial real estate valuation can vary dramatically across seemingly similar assets.

6.6 Capital Abundance and Market Compression

The increasing institutionalization of industrial real estate has had important consequences for investors.

Over the past decade, industrial real estate attracted substantial inflows from pension funds, insurance companies, sovereign wealth funds, and public market investors. This influx of capital increased competition for high-quality assets and contributed to significant cap rate compression in many logistics-oriented markets.

As more capital entered the sector, investors increasingly expanded beyond traditional warehouse acquisitions into specialized industrial subsectors, including cold storage, manufacturing, industrial outdoor storage, and data infrastructure.

However, institutional capital does not move evenly across all market segments. Assets that require specialized underwriting or local market expertise may continue to experience less competition than highly standardized logistics facilities.

This uneven distribution of capital remains one of the defining characteristics of the industrial investment landscape.

6.7 Why Market Structure Matters

Understanding market participants is essential because investor behavior directly influences pricing.

Cap rates are not determined solely by real estate fundamentals. They are also influenced by:

- buyer demand;

- availability of capital;

- financing conditions;

- perceived risk;

- transaction liquidity;

investor specialization.

Two industrial facilities with similar cash flows may trade at significantly different valuations simply because they attract different buyer pools.

A modern distribution facility located in a major logistics hub may attract dozens of institutional bidders. A specialized manufacturing facility in a secondary market may attract only a handful of qualified buyers.

The resulting difference in competition often translates directly into differences in pricing and cap rates.

This observation becomes particularly important in the next chapter, where valuation and cap-rate dynamics are examined in greater detail.

6.8 Key Observations

Industrial real estate ownership is increasingly fragmented across institutional investors, public net-lease REITs, and private sale-leaseback platforms. Each participant operates under different return objectives, underwriting frameworks, and acquisition criteria.

As a result, industrial assets do not compete within a single marketplace. Different buyer groups often pursue different property types, geographic markets, and transaction structures.

Understanding who the buyers are—and which assets they are willing to pursue—is therefore essential for understanding valuation, competition, and investment opportunities within the industrial real estate sector.

The next section explores how these differences ultimately manifest themselves in capitalization rates, valuation frameworks, and risk-adjusted return expectations across the industrial market.

7. Valuation and Cap Rate Dynamics

7.1 Understanding Industrial Real Estate Valuation

Industrial real estate is ultimately valued based on the income it generates and the risk associated with that income. While many factors influence pricing, capitalization rates remain one of the most widely used valuation metrics in commercial real estate.

At its most basic level, a capitalization rate represents the relationship between a property's annual net operating income and its market value.

Cap Rate = Net Operating Income ÷ Property Value

A property generating $1 million of annual net operating income and valued at $20 million would therefore trade at a 5% capitalization rate.

Although the formula itself is simple, cap rates incorporate a broad range of investor expectations regarding risk, liquidity, tenant quality, lease duration, growth prospects, financing conditions, and future exit values.

As a result, cap rates should not be viewed merely as measures of income. They are also measures of investor perception.

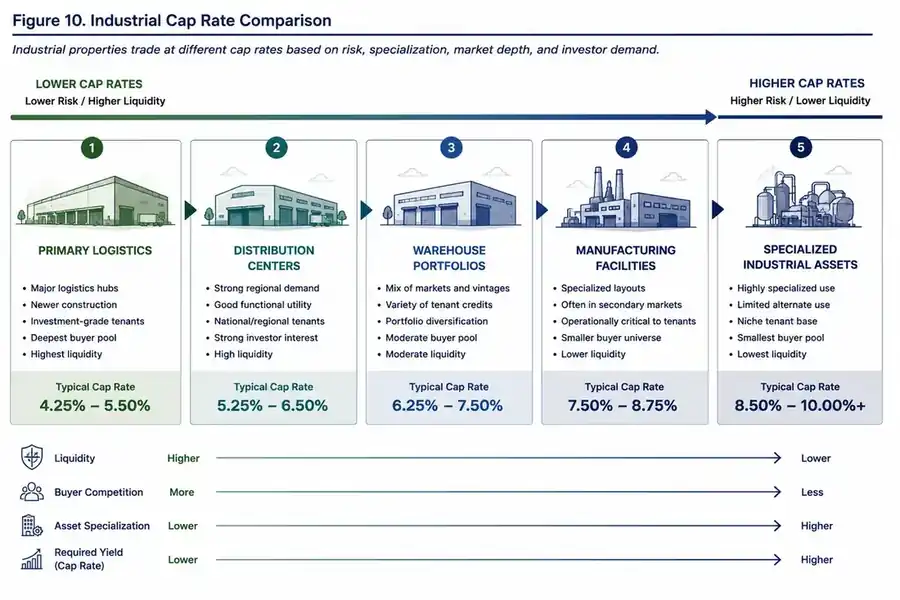

7.2 Why Industrial Cap Rates Vary

One of the most common misconceptions among investors is that all industrial real estate should trade at similar valuations.

In reality, industrial cap rates vary considerably across property types, markets, tenant profiles, and ownership structures.

A newly constructed distribution center leased to an investment-grade tenant in a major logistics market may attract dozens of institutional bidders and trade at a relatively low cap rate. A specialized manufacturing facility located in a secondary market may attract a much smaller buyer pool and therefore trade at a higher cap rate despite generating comparable cash flow.

The difference is not necessarily the income stream itself. More often, it reflects differences in perceived risk and market liquidity.

Investors pay premiums for assets that are easier to finance, easier to sell, and easier to re-lease in the future.

7.3 The Relationship Between Risk and Cap Rates

Cap rates can be viewed as the market's pricing mechanism for risk.

All else being equal, investors generally require higher returns when they perceive greater uncertainty regarding future cash flows or exit values.

This relationship is often represented as a risk-return spectrum.

7.4 Manufacturing Facilities and the Cap Rate Premium

Manufacturing facilities frequently trade at cap rates above those observed for comparable logistics and distribution assets.

Several factors contribute to this premium.

First, manufacturing facilities are often more specialized than traditional warehouse properties. Buildings may contain production infrastructure, customized layouts, utility requirements, environmental systems, or tenant improvements that are difficult to replicate or adapt for alternative users.

Second, manufacturing assets are frequently located in secondary or tertiary markets rather than major logistics hubs. These markets often have fewer active buyers and less transaction liquidity.

Third, investors may perceive manufacturing tenants as carrying greater business risk than large national logistics operators, particularly when tenant credit information is limited.

Finally, the buyer universe for manufacturing assets is often narrower. Reduced competition alone can contribute to higher cap rates.

Importantly, these factors do not necessarily imply inferior asset quality. They simply influence how the market prices risk.

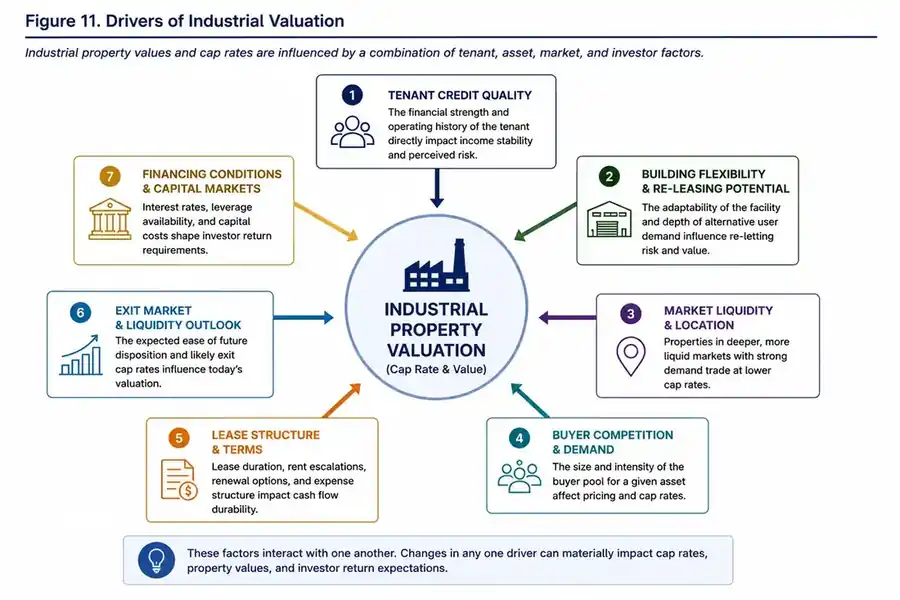

7.5 Tenant Credit as a Valuation Driver

In net-lease and sale-leaseback transactions, investors are often underwriting two assets simultaneously: the building and the tenant.

As a result, tenant credit quality becomes one of the most important determinants of valuation.

Properties leased to large, financially strong tenants often command premium valuations because investors perceive rental income as more durable and predictable.

Conversely, facilities occupied by privately held companies with limited public financial disclosure may trade at higher cap rates even when the underlying business is healthy and profitable.

This phenomenon creates an interesting dynamic within industrial sale-leasebacks. In many cases, valuation differences are driven less by the physical building and more by investor perceptions regarding tenant creditworthiness.

The property may be identical. The tenant profile may determine the pricing.

7.6 Building Flexibility and Re-Leasing Risk

A second major valuation factor is building flexibility.

Industrial investors frequently ask a simple question:

- If the current tenant leaves, who is the next tenant?

For modern warehouses and distribution facilities, the answer may be relatively straightforward. Large pools of potential users often exist, and the building can frequently accommodate a variety of industrial activities.

Manufacturing facilities present a different challenge.

Some manufacturing buildings are highly adaptable and can support multiple users. Others contain specialized configurations that may limit alternative uses without significant capital investment.

The greater the perceived difficulty of re-leasing the facility, the greater the valuation discount investors may apply.

This consideration becomes particularly important when evaluating long-term exit assumptions.

7.7 Market Liquidity and Buyer Competition

Liquidity is another powerful determinant of industrial real estate pricing.

Primary logistics markets attract substantial institutional capital. Large numbers of buyers compete for a relatively limited inventory of institutional-quality assets. This competition tends to compress cap rates and increase valuations.

Secondary-market manufacturing facilities often operate under different conditions. The buyer universe may be smaller, transaction activity may be less frequent, and financing availability may be more limited.

As discussed in the previous chapter, different buyer groups pursue different asset types. The resulting differences in competition often manifest directly in valuation.

In many cases, the cap-rate spread between logistics and manufacturing properties may reflect differences in liquidity as much as differences in underlying business risk.

7.8 Exit Valuation and Investor Expectations

Cap rates also reflect assumptions about future exit opportunities.

When investors purchase industrial assets, they are not only evaluating current income. They are also evaluating the likelihood of selling the property in the future and the pricing they may receive upon exit.

Assets located in highly liquid institutional markets generally offer greater confidence regarding future disposition opportunities. This confidence may justify lower required returns.

By contrast, investors purchasing specialized manufacturing facilities often assume a more limited future buyer universe. The possibility of a narrower exit market can contribute to higher initial cap rates.

This distinction highlights the relationship between liquidity and valuation. Investors frequently pay more today for assets they believe will be easier to sell tomorrow.

The factors discussed throughout this chapter rarely operate independently. Industrial real estate valuations are typically influenced by a combination of tenant characteristics, asset-specific considerations, market conditions, and investor behavior. Figure 11 summarizes the primary drivers that collectively influence industrial property valuation and capitalization rates.

7.9 Risk Premium or Market Inefficiency?

This brings us to one of the central questions of the paper.

Do higher manufacturing cap rates simply represent compensation for higher risk, or do they partially reflect market inefficiencies?

The answer is likely a combination of both.

Certain manufacturing facilities undoubtedly carry higher operational, leasing, and liquidity risks than institutional logistics assets. In those cases, higher cap rates may represent appropriate compensation for additional uncertainty.

However, industrial markets are not perfectly efficient. Specialized knowledge, limited buyer participation, relationship-driven sourcing, and informational asymmetries can create pricing differences that exceed underlying risk differences.

When fewer investors are willing or able to evaluate a particular asset type, opportunities may emerge for investors possessing the expertise necessary to understand those risks more accurately.

This possibility forms one of the key investment theses frequently cited by participants in the industrial sale-leaseback market.

7.10 Key Observations

Industrial cap rates are influenced by far more than current income. Tenant credit, building flexibility, market liquidity, investor competition, and exit expectations all play important roles in determining valuation.

Manufacturing facilities often trade at higher cap rates than logistics-oriented industrial assets, but those higher yields should not automatically be interpreted as evidence of inferior quality. In many cases, they reflect differences in specialization, buyer participation, and perceived liquidity.

The most important question for investors is not whether an asset trades at a higher cap rate. The critical question is whether the additional yield adequately compensates for the underlying risks being assumed.

The next section expands this analysis by examining market size, transaction volume, and the broader opportunity set available within the industrial sale-leaseback market.

8. Market Size and Opportunity Set

8.1 Looking Beyond Current Transaction Volume

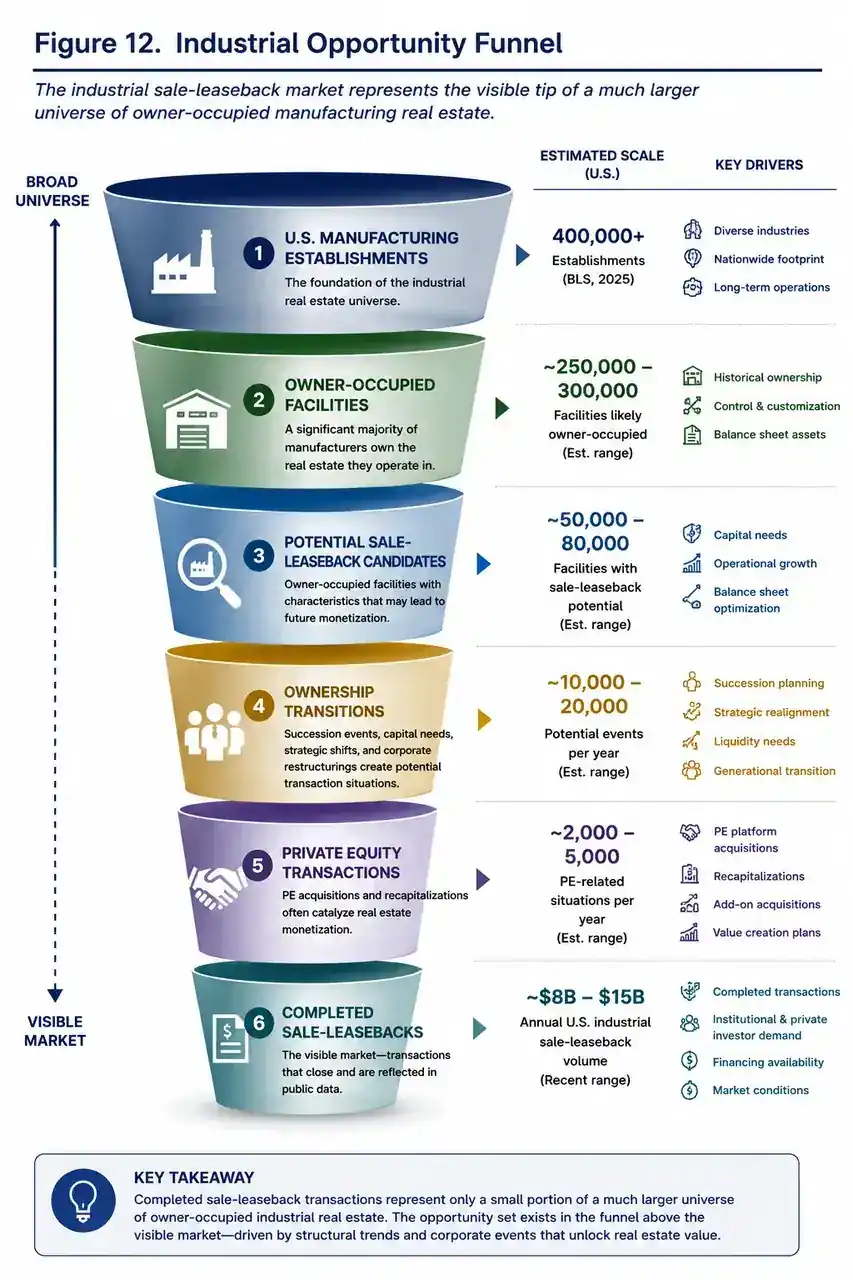

One of the challenges in evaluating the industrial sale-leaseback market is that publicly reported transaction volume may understate the size of the underlying opportunity set.

Most market statistics focus on completed transactions. Analysts can observe acquisitions, dispositions, leasing activity, financing events, and sale-leaseback transactions once they occur. However, these datasets provide limited visibility into the much larger universe of owner-occupied industrial properties that have not yet entered the transaction market.

As discussed earlier in this paper, a substantial portion of manufacturing activity continues to take place within facilities owned by the businesses that occupy them. These properties often remain outside institutional real estate ownership structures for decades.

Consequently, the future opportunity set may be measured not only by current transaction volume but also by the scale of industrial real estate that remains embedded within operating businesses.

This distinction is important because it suggests that the industrial sale-leaseback market may be far larger than annual transaction statistics imply.

8.2 The Scale of Owner-Occupied Industrial Real Estate

The United States contains hundreds of thousands of manufacturing establishments distributed across a broad range of industries and geographic regions.

Many of these businesses continue to own the facilities from which they operate. While comprehensive national ownership statistics remain difficult to obtain, the persistence of owner-occupied manufacturing facilities is evident throughout the industrial economy.

For many business owners, real estate ownership was never part of a deliberate investment strategy. Facilities were acquired to support production, warehousing, processing, or distribution activities. Over time, appreciation in industrial property values transformed these facilities into significant balance sheet assets.

The result is a large inventory of industrial real estate that exists outside traditional institutional ownership channels.

From an investment perspective, these facilities represent potential future transaction opportunities rather than immediately available inventory.

That distinction may be one of the defining characteristics of the industrial sale-leaseback market.

8.3 Reshoring and Domestic Manufacturing Investment

Recent developments in industrial policy have increased investor attention on domestic manufacturing capacity.

Supply chain disruptions, geopolitical considerations, labor availability concerns, and national security priorities have all contributed to renewed interest in domestic production capabilities.

As companies invest in new facilities, expand existing operations, and modernize production infrastructure, industrial real estate becomes increasingly important as a strategic corporate asset.

These trends may influence both the quantity and quality of future sale-leaseback opportunities.

Some businesses may require capital to fund expansion initiatives. Others may seek ways to finance modernization projects while preserving operational continuity. In both cases, industrial real estate can become an important source of liquidity.

The relationship between manufacturing investment and industrial real estate monetization may therefore become increasingly significant over the coming decade.

8.4 Private Equity as a Transaction Catalyst

As discussed in Section 5, private equity activity has become an important driver of industrial sale-leaseback transactions.

Ownership transitions frequently create opportunities to separate operating assets from real estate assets. When sponsors acquire manufacturing businesses, they often evaluate whether real estate ownership contributes meaningfully to value creation or whether capital can be deployed more effectively elsewhere.

This dynamic can generate transaction opportunities that would otherwise never emerge.

Importantly, the catalyst is frequently a corporate event rather than a real estate event. The property becomes available because ownership of the business changes, not because ownership of the real estate changes.

As private equity activity continues across the middle market, this mechanism may remain a significant source of industrial sale-leaseback volume.

8.5 Succession Planning and Demographic Transitions

Another often-overlooked source of industrial real estate transactions is business succession planning.

Many manufacturing businesses remain privately owned and founder-led. In numerous cases, ownership structures have remained unchanged for decades.

As business owners approach retirement, questions surrounding ownership transition, liquidity, estate planning, and business continuity become increasingly important.

Real estate frequently plays a central role in these discussions.

A sale-leaseback can provide liquidity while preserving operational continuity. It can also simplify ownership transitions by separating the operating company from real estate ownership.

Because demographic transitions occur gradually, succession-related opportunities often emerge steadily rather than cyclically.

For investors, this creates a transaction pipeline driven by long-term structural trends rather than short-term market conditions.

8.6 Capital Allocation as a Long-Term Driver

Perhaps the most durable driver of industrial sale-leaseback activity is capital allocation.

Business owners continually evaluate how capital is deployed across the enterprise. Equipment upgrades, automation initiatives, acquisitions, debt reduction, and growth investments all compete for available resources.

Real estate ownership represents one possible use of capital.

A sale-leaseback allows management teams to reconsider that allocation decision without disrupting operations.

As financial sophistication increases and alternative capital sources become more widely available, more businesses may evaluate whether ownership of industrial real estate remains the most productive use of capital.

This question exists regardless of interest rates, economic cycles, or transaction volumes.

As a result, capital allocation considerations may represent one of the most persistent long-term drivers of industrial sale-leaseback activity.

8.7 The Difference Between Inventory and Opportunity

One of the most important distinctions in industrial real estate is the difference between available inventory and potential opportunity.

Traditional industrial investors often evaluate assets currently available for acquisition.

Sale-leaseback investors frequently evaluate assets that are not for sale today but may become available in the future due to:

- ownership transitions;

- private equity acquisitions;

- succession events;

- capital needs;

- expansion initiatives;

balance sheet optimization.

This difference fundamentally changes how market size should be measured.

The relevant universe is not simply the volume of assets currently trading.

It is the volume of assets that could potentially transact under the right circumstances.

Figure 12 illustrates how the visible sale-leaseback market represents only a small portion of a much larger universe of owner-occupied industrial facilities. Most industrial properties never enter the transaction market, and sale-leaseback opportunities often emerge only when triggered by ownership transitions, private equity activity, succession planning, or capital allocation decisions.

8.8 Can Manufacturing Real Estate Be an Underfollowed Asset Class?

This paper began with a simple observation: industrial real estate is often discussed through the lens of logistics, distribution, and warehouse markets.

Those sectors undoubtedly deserve attention. However, they represent only part of the broader industrial ecosystem.

Manufacturing facilities occupy a different position within the market. They frequently remain owner-occupied, operate outside institutional ownership channels, and attract fewer investors than traditional logistics assets.

This raises an important question.

If large portions of U.S. manufacturing real estate remain embedded within operating businesses, and if future ownership transitions continue to generate sale-leaseback opportunities, could manufacturing real estate represent one of the largest underfollowed segments of private real estate?

The answer remains open to debate. However, the evidence presented throughout this paper suggests that the opportunity set may be substantially larger than many investors currently recognize.

8.9 Key Observations

The size of the industrial sale-leaseback market cannot be measured solely through completed transaction volume. A significant portion of the opportunity set exists within owner-occupied industrial real estate that remains outside traditional institutional ownership structures.

Long-term trends including reshoring, manufacturing investment, private equity activity, succession planning, and corporate capital allocation may all contribute to future transaction volume.

Taken together, these forces suggest that the potential market for industrial sale-leaseback transactions may be considerably larger than the currently visible transaction market.

For investors willing to analyze operating businesses in addition to real estate assets, owner-occupied manufacturing facilities may represent one of the most significant and least understood opportunity sets within private real estate.

9. Risks and Investment Considerations

9.1 Understanding Risk in Industrial Sale-Leaseback Investments

Every investment opportunity exists somewhere on a risk-return spectrum. Industrial sale-leaseback transactions are no exception.

Throughout this paper, we have discussed how specialized manufacturing facilities often trade at higher capitalization rates than traditional logistics assets. While these higher yields may appear attractive, investors should recognize that cap-rate premiums generally reflect some combination of additional risk, reduced liquidity, or increased uncertainty.

The objective of underwriting is therefore not to eliminate risk. Rather, it is to determine whether the compensation received is sufficient for the risks assumed.

This distinction is particularly important in industrial sale-leaseback investing, where investors frequently underwrite both the physical real estate and the operating business occupying the property.

9.2 Tenant Credit Risk

Tenant credit quality is often the single most important risk factor in a sale-leaseback transaction.

Unlike multi-tenant properties, many industrial sale-leaseback investments depend on the performance of a single operating business. If the tenant experiences financial distress, operational challenges, industry disruption, or bankruptcy, the value of the investment may be materially affected.

This risk is particularly relevant when evaluating privately held manufacturing businesses, which often provide less public financial information than publicly traded companies.

Investors should therefore evaluate:

- profitability trends;

- leverage levels;

- cash flow stability;

- customer concentration;

- supplier dependencies;

- management quality;

industry positioning.

In many cases, understanding the tenant may be more important than understanding the building.

9.3 Facility Specialization Risk

Industrial facilities vary significantly in their adaptability.

Some properties can accommodate a wide range of industrial users with minimal modifications. Others contain highly specialized infrastructure, production layouts, environmental controls, utility requirements, or equipment configurations that limit their appeal to alternative tenants.

The more specialized a facility becomes, the smaller the potential future tenant pool may be.

This creates what is often referred to as re-leasing risk.

If the current tenant vacates, investors may face longer vacancy periods, higher capital expenditures, or lower rental rates than originally anticipated.

Consequently, facility specialization is one of the primary reasons certain industrial assets trade at higher cap rates than conventional logistics properties.

9.4 Geographic Concentration Risk

Location influences not only operational performance but also investment liquidity.

Industrial facilities located in major logistics hubs often benefit from deep tenant demand, active transaction markets, and broad investor participation.

Facilities located in smaller manufacturing markets may operate under different conditions. While these markets may offer higher stated yields, they can also experience lower transaction volume, fewer qualified buyers, and greater dependence on local economic conditions.

Geographic concentration becomes particularly important when multiple assets are clustered within a single region.

Investors should evaluate whether regional economic conditions, labor market dynamics, infrastructure investment, and local industry exposure could materially affect portfolio performance.

9.5 Industry Concentration Risk

Manufacturing is not a single industry.

Industrial tenants may operate in sectors including aerospace, food processing, packaging, chemicals, automotive components, industrial machinery, electronics, medical devices, and numerous other categories.

Each industry possesses unique economic drivers, competitive pressures, and cyclical characteristics.

A portfolio heavily concentrated in one industry may be exposed to sector-specific risks that are not immediately apparent when evaluating individual properties.

For example, regulatory changes, technological disruption, supply-chain shifts, commodity price volatility, or changing consumer demand could disproportionately affect certain manufacturing sectors.

Diversification across industries can therefore play an important role in managing portfolio risk.

9.6 Refinancing and Capital Markets Risk

Industrial real estate valuations are influenced by broader capital market conditions.

Changes in interest rates, lending standards, debt availability, and financing costs can significantly affect property values and transaction activity.

Assets acquired during periods of abundant capital may face different refinancing conditions when debt matures.

Investors should therefore consider:

- debt maturity schedules;

- fixed versus floating-rate exposure;

- lender concentration;

- refinancing assumptions;

future capital requirements.

While these factors affect all commercial real estate sectors, specialized industrial properties may experience greater sensitivity because financing options can be more limited than for highly liquid institutional assets.

9.7 Exit Liquidity Risk

Investment returns are influenced not only by current cash flow but also by future exit opportunities.

Properties located in highly liquid institutional markets generally benefit from large pools of potential buyers and more predictable pricing.

Specialized manufacturing facilities may attract a narrower buyer universe.

As discussed in previous sections, different investor groups pursue different types of industrial assets. When fewer buyers are willing or able to acquire a property, future disposition options may become more limited.

Exit liquidity risk does not necessarily imply poor investment performance. However, it should be considered when evaluating expected holding periods, valuation assumptions, and return expectations.

Investors often receive higher initial yields precisely because future liquidity is less certain.

9.8 Environmental and Regulatory Exposure

Industrial properties may face environmental risks that are less common in other commercial real estate sectors.

Manufacturing activities can involve chemicals, fuels, solvents, waste streams, emissions, and other operational considerations that may create environmental liabilities.

While modern environmental regulations and due diligence procedures help mitigate these risks, investors should carefully evaluate:

- Phase I environmental reports;

- Phase II investigations where applicable;

- remediation history;

- regulatory compliance;

- groundwater concerns;

hazardous materials management.

Environmental issues can affect financing availability, future disposition opportunities, operating costs, and property values.

As a result, environmental due diligence remains a critical component of industrial underwriting.

9.9 Risk Interactions and Portfolio Construction

One of the most important observations in industrial investing is that risks rarely occur independently.

A specialized manufacturing facility located in a secondary market and occupied by a privately held tenant may simultaneously expose investors to:

- tenant credit risk;

- facility specialization risk;

- geographic concentration risk;

liquidity risk.

Conversely, strengths in one area may offset weaknesses elsewhere. A highly specialized facility may still represent an attractive investment if supported by a strong tenant, favorable lease structure, and mission-critical operational importance.

Effective underwriting therefore requires evaluating the interaction among risks rather than analyzing each factor in isolation.

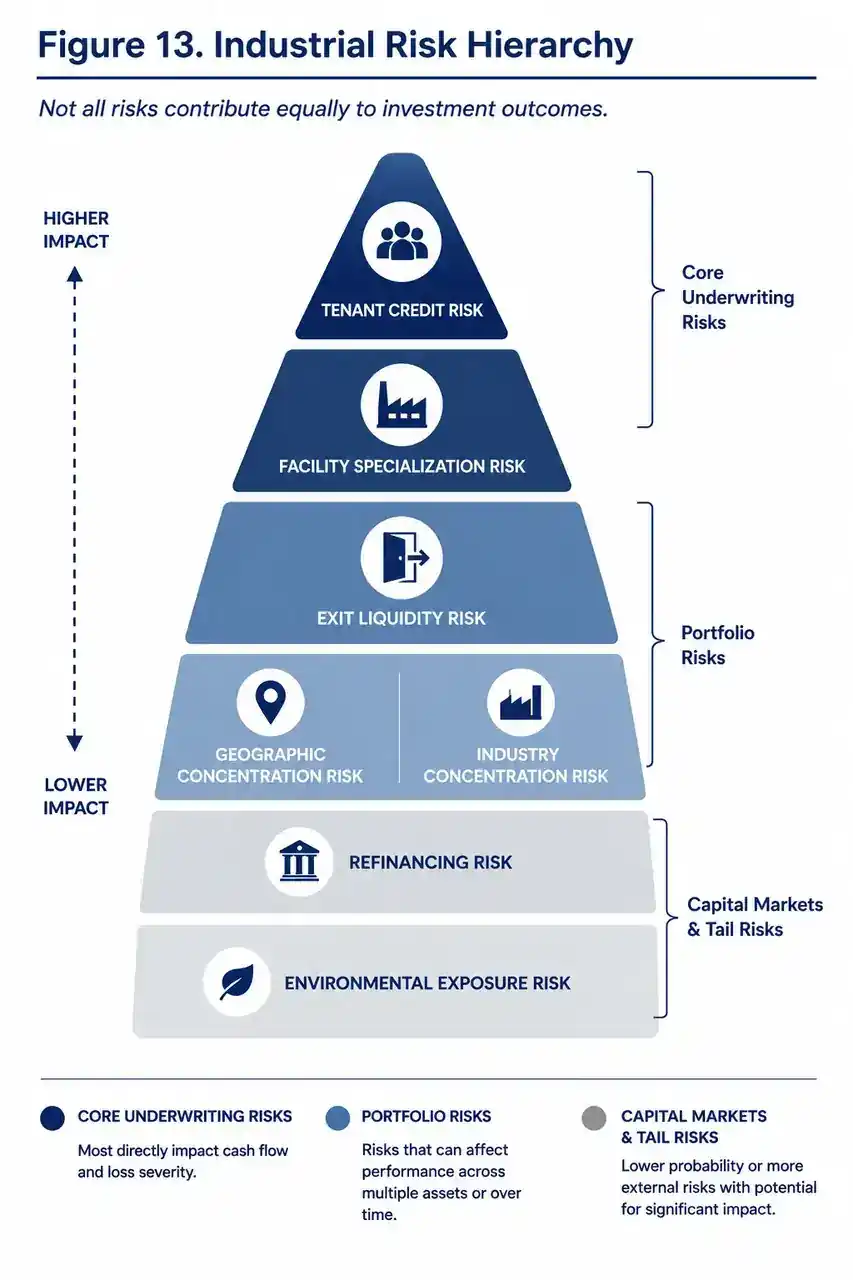

Industrial sale-leaseback investments are exposed to multiple risk categories that vary in both probability and potential impact. Tenant credit quality and facility specialization typically represent the most significant underwriting considerations, while environmental exposure, although less frequent, may carry substantial downside consequences. Effective portfolio construction requires evaluating both individual risks and their interactions.

9.10 Key Observations

Industrial sale-leaseback investments can provide higher stated yields, but those yields should be understood within the context of the risks being assumed.

Tenant credit quality, facility specialization, geographic concentration, industry exposure, refinancing conditions, exit liquidity, and environmental considerations all influence investment outcomes.

Higher cap rates do not automatically indicate superior opportunities. In many cases, they reflect additional risk, reduced liquidity, or increased uncertainty.

The central challenge for investors is therefore not identifying assets with the highest yields, but determining whether the additional yield adequately compensates for the underlying risks.

That distinction ultimately separates successful underwriting from simple yield chasing.

Section 10

Case Study: Industrial Sale-Leaseback Strategy in Practice

10. Case Study: Industrial Sale-Leaseback Strategy in Practice

10.1 Introduction

The preceding chapters examined the industrial sale-leaseback market from a broader industry perspective, including market structure, ownership trends, valuation dynamics, transaction drivers, and investment risks.

This chapter applies that framework to a specific industrial real estate investment strategy using sponsor-provided materials for MAGCP Industrial Fund III, LP.

The objective is not to evaluate the merits of the investment itself, nor to provide investment recommendations. Rather, the purpose is to examine how an active industrial sale-leaseback investment platform implements the concepts discussed throughout this paper.

All observations in this chapter are derived exclusively from sponsor-provided materials reviewed as part of this research.

10.2 Strategy Overview